The total expanded polystyrene (EPS) market is expected to grow at a CAGR of 5.3% from 2017-2023 and reach $ 19.9 billion by 2023. Increasing population and urbanization in developing countries such as India, Thailand, Brazil, etc. have resulted in the growth of manufacturing sectors such as automotive, packaging, and building & construction. This growth in different industries coupled with the huge demand for packaging solutions in the food and beverage & medical and pharmaceutical sector to enhance product safety and freshness of packaged food and medicines during transportation largely drive the EPS market growth.

In terms of types of EPS, white EPS accounted for the largest market share in 2017, followed by black and grey EPS. White EPS exhibits superior mechanical durability and water resistant properties, which make it suitable for various end-use industries.

EPS finds its heavy utility in the building and construction sector. In 2017, the packaging and building & construction sectors emerged as the leading end use industries capturing market share. Major packaging applications include retail, food, and consumer goods. The rising demand for EPS in cold chain packaging solutions is expected to drive the market for EPS in the packaging sector. Its applications in the building and construction sector include insulated panel systems for walls, roofs, and floors as well as facades for both domestic and commercial buildings. Rising growth in the building and construction industry will eventually result in the growth of the EPS market. Automotive is another significant end use industry for EPS.

Asia-Pacific was the most favoured market for EPS in 2017 that bagged the largest market share. The region is expected to grow at the fastest rate of 6.3% from 2017-2023 that will remain the leading market in 2023 as well. China subjugated the EPS market in Asia-Pacific due to the growing electrical and electronic and packaging application in the country. A shift of manufacturing companies to India, China, Indonesia, etc., has been observed because of the availability of low cost labour and raw materials.

The demand for EPS in North America and Europe has been anticipated to grow at a moderate rate. EPS is banned in food packaging applications in several states of the U.S. as EPS waste causes tremendous trouble when it leaks into marine environments and contaminates water.

However, EPS recycling techniques are now trending in Europe. Greenmax, DUE Recycling Systems, etc., are the companies that provide solutions to recycle EPS.

The market is highly fragmented due to the presence of a large number of EPS manufacturers. Companies are working closely with consumers to address their need regarding EPS and with their latest R&D companies that are designing EPS products with exceptional properties. In 2014, BASF started to use an innovative flame retardant “PolyFr”. All of BASF’s Styropor, Neopor, and Styrodur polystyrene products for the European market have better flame retardant properties than HBCD (hexabromocyclododecane), which was used in the past. Some of the major players that operate in this market are BASF, SABIC, INEOS, Total SA, Nova Chemicals Corporation, Synthos S.A., Alpek S.A.B. De Cv, PJSC Sibur Holding, ACH Foam Technologies Inc., Versalis S.P.A, Nova Chemicals Corporation, Synbra Holding BV and Flint Hills Resources, LLC, & others.

1 Introduction

1.1 Goal & Objective

1.2 Report Coverage

1.3 Supply Side Data Modelling & Methodology

1.4 Demand Side Data Modelling & Methodology

2 Executive Summary

3 Market Outlook

3.1 Introduction

3.2 Current & Future Outlook

3.3 DROC

3.3.1 Drivers

3.3.1.1 Demand Drivers

3.3.1.2 Supply Drivers

3.3.2 Restraints

3.3.3 Opportunities

3.3.4 Challenges

3.4 Market Entry Matrix

3.5 Market Opportunity Analysis

3.6 Market Regulations

3.7 Pricing Mix

3.9 Value Chain & Ecosystem

3.8 Key Customers

4 Demand Side Analysis

4.1 Expanded Polystyrene (EPS) Market by Type

4.1.1 White Expanded Polystyrene (EPS)

4.1.2 Black Expanded Polystyrene (EPS)

4.1.3 Grey Expanded Polystyrene (EPS)

5 Expanded Polystyrene (EPS) Market, By Application

5.1.1 Packaging

5.1.1.1 Loose Fill Packaging

5.1.1.2 Transport Packaging

5.1.1.4 Protective & Display packaging

5.1.2 Building & Construction

5.1.2.1 Insulated panel systems

5.1.2.2 Floors, Walls & Ceilings

5.1.2.3 Roofing system

5.1.2.4 Insulating Concerte Foam (ICF)

5.1.2.5 External Insulating & Finishing Systems

5.1.3 Electrical & Electronics

5.1.4 Automotive

5.1.5 Others

Pipe Insulation

Poultry Houses

Cold Air Storages

6 Expanded Poystyrene Market Analysis, By Region

6.1 North America

6.1.1 U.S.

6.1.2 Canada

6.1.3 Mexico

6.2 Europe

6.2.1 Germany

6.2.2 Italy

6.2.3 France

6.2.4 Spain

6.2.5 UK

6.2.6 Poland

6.2.7 Turkey

6.2.8 Rest of Europe

6.3 Asia Pacific

6.3.1 China

6.3.2 Japan

6.3.3 India

6.3.4 Malyasia

6.3.5 Thailand

6.3.6 Idonesia

6.3.7 Rest of APAC

6.4 Middle East & Africa

6.4.1 Saudi Arabia

6.4.2 UAE

6.4.5 Rest Of Middle East & Africa

6.5 South America

6.5.1 Brazil

6.5.3 Argentina

6.5.4 Rest of South America

7 Supply Side Analysis

7.1 Strategic Benchmarking

7.1 Market Share Analysis

7.1 Key Players

7.3.1 BASF

7.3.2 Dow Chemical Co.

7.3.3 SABIC

7.3.4 INEOS

7.3.5 Total SA

7.3.6 Nova Chemicals Corporation

7.3.7 Synthos S.A.

7.3.8 Alpek S.A.B. De Cv

7.3.9 PJSC Sibur Holding

7.3.10 ACH Foam Technologies Inc.

7.3.11 Versalis S.P.A

7.3.12 Nova Chemicals Corporation

7.3.13 Synbra Holding BV

7.3.14 Flint Hills Resources, LLC & Others

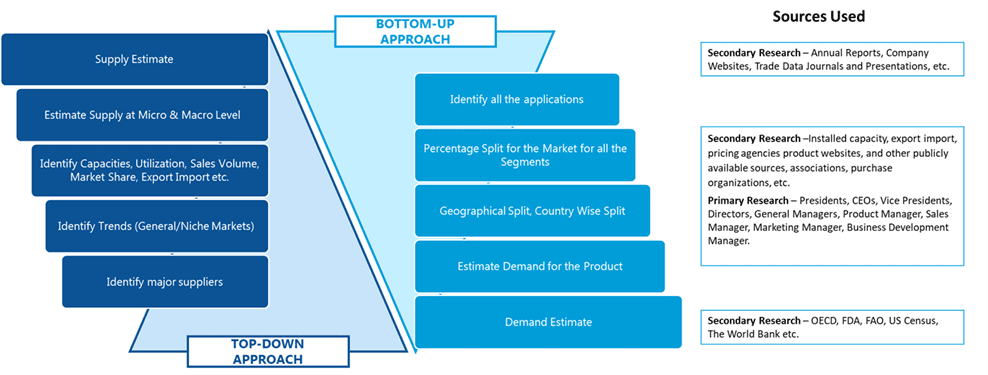

SDMR employs a three way data triangulation approach to arrive at market estimates. We use primary research, secondary research and data triangulation by top down and bottom up approach

Secondary Research:

Our research methodology involves in-depth desk research using various secondary sources. Data is gathered from association/government publications/databases, company websites, press releases, annual reports/presentations/sec filings, technical papers, journals, research papers, magazines, conferences, tradeshows, and blogs.

Key Data Points through secondary research-

Macro-economic data points

Import Export data

Identification of major market trends across various applications

Primary understanding of the industry for both the regions

Competitors analysis for the production capacities, key production sites, competitive landscape

Key customers

Production Capacity

Pricing Scenario

Cost Margin Analysis

Key Data Points through primary research-

Major factors driving the market and its end application markets

Comparative analysis and customer analysis

Regional presence

Collaborations or tie-ups

Annual Production, and sales

Profit Margins

Average Selling Price

Data Triangulation:

Data triangulation is done using top down and bottom approaches. However, to develop accurate market sizing estimations, both the methodologies are used to accurately arrive at the market size. Insert Image